Mr. Petrov, a new owner of the Zorro insurance company, discovered in his office a folder left behind after the meeting by one of top managers. From the reports found in the folder, it became clear that Mr. Petrov had been intentionally deceived through distorting the company's key ratios. In particular, it became obvious from the contents of the discovered documents that approved budget had been implemented only on paper for two years prior to purchasing a company by Mr. Petrov, who applied for Insurance Forensic in order to:

- understand the current situation (real financial results of the Zorro insurance company);

- detect the mechanisms that had been used for obtaining and demonstrating “fine” results;

- find the persons involved in the detected corporate fraud;,

- elaborate measures that would prevent and counteract such fraud schemes in future.

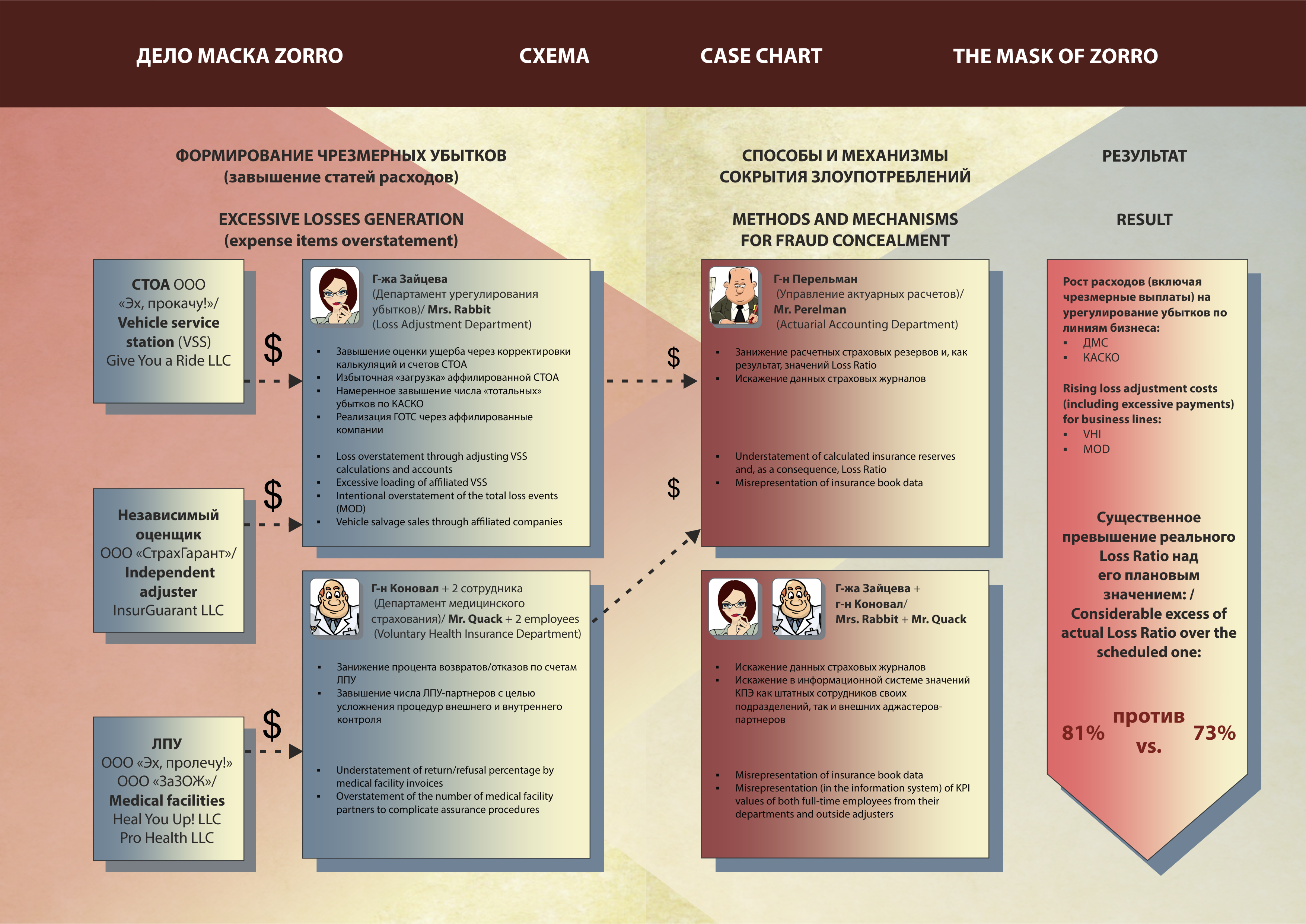

STEP 1

The verification of the correctness of the insurance reserve calculation has shown that the Chief Actuary Mr. Perelman intentionally understated the total insurance reserves in collusion (as turned out later) with other company employees concerned (namely, one of the underwriters together with Mrs. Rabbit, Head of Loss Adjustment Department), by using the following methods:

- intentional application of mathematical calculation methods that allowed obtaining the most “optimistic” (understated) evaluation of insurance reserves;

- excessive and abusive application of so called expert appraisals, assumptions and estimates;

- fraudulent misrepresentation of insurance book data;

- substitution of underwriting Loss Ratio for actuarial (calendar) Loss Ratio;

- segmentation of the key calculated rates into those calculated before and after the date of purchasing a company by Mr. Petrov, thus capitalizing on the fact of the change of ownership in the middle of a calendar year.

As a result, the above manipulations with the insurance reserve calculation made it possible to intentionally understate the total Loss Ratio by staying within values acceptable to company management (not exceeding 70-73% in accordance with Mr. Petrov’s expectations).

STEP 2

The Closed File Review has detected the following manipulations made by Mrs. Rabbit's behest:

- regular misrepresentation of the data from insurance loss book and RBNS book and, consequently, fudging the ratios evaluating the operational efficiency of outside adjusters to get desirable results (average payments for business lines, average loss adjustment terms, etc.);

- intentional delay in attaching (via accounting system) the incurred losses to insurance contracts and in entering other data, thus allowing the payment of compensation through encashed retirement in circumvention of authorized procedures;

- artificial restriction of the number of the participants in vehicle salvage auctions thus making it possible to win the auction for the companies affiliated with the insurance company employees and/or outside adjusters (such as Give You a Ride! LLC founded by Mrs. Rabbit's brother).

STEP 3

While adjusting the Fraud Detection & Prevention System (FDPS) and implementing some computer forensics procedures it has been found that lack of appropriate control over calculation of insured losses frequently resulted in excessive unfounded payments. For instance, Mr. Quack, Head of Voluntary Health Insurance Department (VHI), ignored the authorized procedures for the survey of the invoices raised by medical facility partners.

This was done in collusion with the two employees whose involvement was detected through the comparative analysis of KPI among the VHI employees and then confirmed by examining the data from their mobile devices. Furthermore, when settling MOD (Motor Own Damage) losses, the gross loss was generally extended to total insured loss through the collusion of Mrs. Rabbit and an outside company InsurGuarant LLC regarded as a “reputable” adjuster.

As a result of fraud investigation, we have detected a considerable excess of actual Loss Ratio (portfolio average) over the approved scheduled one (81% vs. maximum permissible 73%). In addition, the detection of the employees involved in fraud afforded to initiate staff restructuring (as a necessary way for suspending fraudulent actions) and revision of relations with “friendly” contractors.

{kind=link}