The Japanese Delight restaurant (hereinafter referred to as “Restaurant”) was facing substantial shortfall, an increasing number of complaints on the Internet and high personnel turnover, in the last six months. It is interesting to note that no significant changes were perceived in the Restaurant's operating activities that could have such deplorable consequences. The restaurant owner, Mr. Hospitable, initiated an independent investigation to detect possible fraud schemes that could be primary cause for worsening the financial results and the image of his Restaurant.

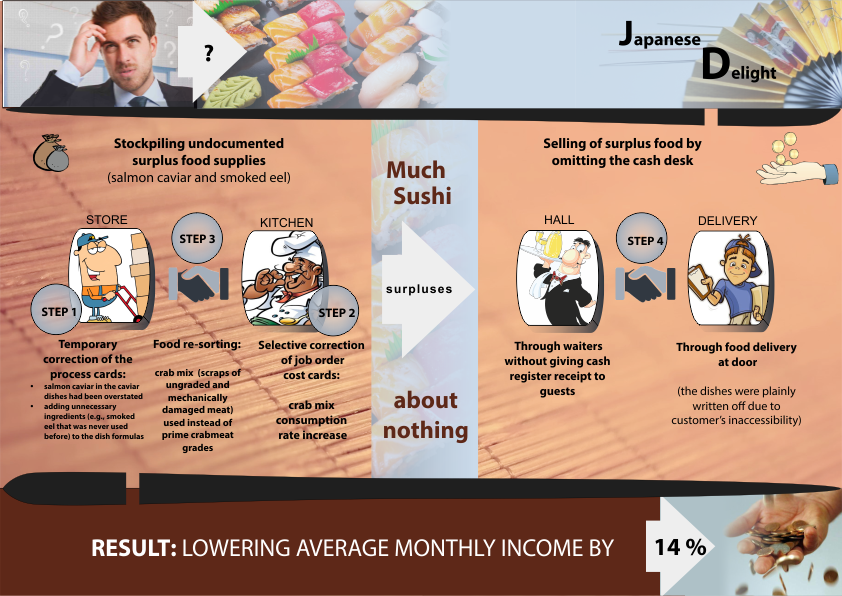

STEP 1

The analysis of the ACS information logging and the revision history of the process cards made it possible to detect the following fraudulent operations of the restaurant staff, aimed at stockpiling undocumented surplus food (salmon caviar and smoked eel) supplies:

Selective correction of job order cost cards. In particular, it was detected that in the last four months the final yield (by weight) of the salmon caviar in the caviar dishes had been overstated in the job order cost cards by 20-25%. The actual food technology remained unchanged, with the volume of purchases being, on the other hand, set too high.

Some process cards were changed through adding unnecessary, extrinsic ingredients (e.g., smoked eel that was never used before) to the dish formulas. It should be noted that such ingredients were never added to the dishes.

STEP 2

The analysis of the complaint book within the last months revealed not only the increase of customers' complaints but also the focus on the dishes with the crabmeat as the base ingredient. The process audit of crabmeat dishes brought to light the problem of food re-sorting with the so-called crab mix (scraps of ungraded and mechanically damaged meat) used instead of prime crabmeat grades (first and second phalanges, knees, rose). The crab mix purchase price was 55 to 70% lower as compared to the prime crabmeat grade price.

The available food re-sorting problem was corroborated by the analysis of data uploads: despite the drop in sales of crab mix dishes (seafood salads, soups, etc.) the crab mix consumption miraculously increased (as it turned out later) due to job order cost card manipulations.

It is worth noting that chief cook, Mr. Liar, explained the increased crab mix consumption by deterioration of crab mix quality in new consignments that allegedly made the chief cook to increase waste food percentage in the inventory accounting database. However, the analysis could not detect neither change of suppliers nor change of storage conditions to support Mr. Liar's arguments.

STEP 3

The synchronization of the above events with the restaurant staff employment dates revealed the existence of correlation between the approximate date of the commencement of the fraudulent manipulations and the commencement date of employment of a new store man, Mr. Horder.

Furthermore, the analysis of affiliation of other restaurant employees (by using, inter alia, social media data) revealed that the store man maintained friendly relations with the Restaurant's chief cook, whose participation should be vital for the implementation of the above schemes of stockpiling surplus food supplies.

STEP 4

The analysis of the information on the sales of dishes having the ingredients, with their consumption distorted to allow stockpiling of unaccounted surpluses, revealed the following mechanisms for selling the above surplus supplies of salmon caviar, smoked eel and prime crabmeat grades:

- The major part of surpluses (mainly caviar and crabmeat) was sold in the restaurant hall mainly through the cancellation of prechecks with corresponding dishes in cases when customers were unwilling to wait for a receipt from a waiter.

- The remaining part of surpluses was sold through food delivery at door. The dishes were plainly written off under the pretext that customers allegedly did not take a call or did not open a door, etc.).

Therefore, we revealed a scheme of stockpiling the surplus food supplies through job order cost card manipulations and food re-sorting with the subsequent selling of food by omitting the cash desk, as well as through unjustified write-off of the food delivery orders. This scheme was functioning owing to a secret deal of the restaurant employees, namely, chief cook, Mr. Liar, and store man, Mr. Horder, as well as waiters and delivery agents. The negative effect of the implementation of this scheme consisted in lowering Mr. Hospitable's average monthly income by 14%.

{kind=link}